Individuals, HUF, AOP, BOI

- No change in Tax Rate

a) For a resident senior citizen (who is 60 yrs or more at any time during the previous but less than 80 yrs on the last day of the previous year)

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Upto Rs.

3,00,000 |

Nil | Nil | Nil |

| Rs. 3,00,000 – Rs. 5,00,000 | 5% of (total income minus Rs. 3,00,000) | Nil | 4% of income tax inclusive of surcharge |

| Rs. 5,00,000 – Rs. 10,00,000 | Rs. 10,000 + 20% of

(total income minus Rs. 5,00,000) |

Nil | 4% of income tax inclusive of surcharge |

| Rs. 10,00,000 –

Rs. 50,00,000 |

Rs. 1,10,000 + 30% of

(total income minus Rs. 10,00,000) |

Nil | 4% of income tax inclusive of surcharge |

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Rs. 50,00,000 –

Rs. 1,00,00,000 |

Rs. 13,10,000 + 30% of

(total income minus Rs. 50,00,000) |

10% of income tax | 4% of income tax inclusive of surcharge |

| Above Rs. 1,00,00,000 | Rs. 28,10,000 + 30% of

(total income minus Rs. 100,00,000) |

15% of

income tax |

4% of income tax and surcharge |

b) For a resident super senior citizen (who is 80 yrs or more at any time during the previous year)

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Upto Rs. 5,00,000 | Nil | Nil | Nil |

| Rs. 5,00,000 – Rs. 10,00,000 | 20% of (total income minus Rs. 500,000) | Nil | 4% of income tax inclusive of surcharge |

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Rs. 10,00,000 –

Rs. 50,00,000 |

Rs. 100,000 + 30% of

(total income minus Rs. 10,00,000) |

Nil | 4% of income tax inclusive of

surcharge |

| Rs. 50,00,000 –

Rs. 100,00,000 |

Rs.13,00,000 + 30% of

(total income minus Rs. 50,00,000) |

10% of income tax | 4% of income tax inclusive of surcharge |

| Above Rs. 100,00,000 | Rs. 28,00,000 + 30% of

(total income minus Rs. 100,00,000) |

15% of

income tax |

4% of income tax inclusive of surcharge |

c) For any other resident individual, any non-resident individual, every HUF / AOP / BOI / artificial juridical person–

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Upto Rs. 2,50,000 | Nil | Nil | Nil |

| Rs. 2,50,000 – Rs. 5,00,000 | 5% of (total income minus Rs. 2,50,000) | Nil | 4% of income tax inclusive of surcharge |

| Net Income range | Income tax rates | Surcharge | Health and Education Cess |

| Rs. 500,000 – Rs. 10,00,000 | Rs. 12,500 + 20% of

(total income minus Rs. 5,00,000) |

Nil | 4% of income tax inclusive of surcharge |

| Rs. 10,00,000 – Rs. 50,00,000 | Rs. 1,12,500 + 30% of

(total income minus Rs.10,00,000) |

Nil | 4% of income tax inclusive of surcharge |

| Rs. 50,00,000 –

Rs. 1,00,00,000 |

Rs. 13,12,500 + 30% of

(total income minus Rs. 50,00,000) |

10% of

income tax if income exceeds Rs 50,00,000 |

4% of income tax inclusive of surcharge |

| Above Rs.

1,00,00,000 |

Rs. 28,12,500 + 30% of

(total income minus Rs. 100,00,000) |

15% of

income tax |

4% of income tax inclusive of surcharge |

- It is proposed to provide a standard deduction of Rs 40,000 for salaried employees irrespective of the salary However, benefit of transport allowance of Rs 19,200 (except in case of differently abled persons) and Medical Reimbursement of Rs 15,000 under Section 17(2) of the Income-tax Act, 1961 (“the Act”) are being withdrawn.

- Any receipt whether capital or revenue in nature arising on account of any re- negotiation, termination or modification in the terms of any contract relating to employment shall be taxable as other income under section 56 of the

- Section 80D of the Act is proposed to be amended to raise the monetary limit of deduction from Rs 30,000 to Rs 50,000 in respect of premium paid for health insurance premium and medical treatment. Further, where insurance policies having cover of more than one year, it is proposed that the deduction shall be allowed on proportionate basis for the number of years for which health insurance cover is provided. The proposed enhanced limit will apply from AY 2019-20.

- Section 80DDB of the Act provides enhanced deduction to senior citizens for medical treatment of specified diseases. It is proposed to amend the provisions of section 80DDB of the Act so as to raise this monetary limit of deduction to Rs 1,00,000 for both senior citizens and very senior citizens. The proposed enhanced limit will apply from AY 2019-1

- A new section 80TTB from AY 2019-20 is proposed to be inserted to provide exemption to senior citizens (exceeding 60 years of age) from deduction of TDS on interest received up to Rs 50,000 from banks, FD, Terms

- Limit for withholding tax under section 194A on the interest payable to senior citizen exceeded from Rs 10,000 to Rs 50,000. Thus, where interest income is received by a senior citizen, no tax will be withheld upto Rs 50,000. Further, where the senior citizen is earning that interest on behalf of HUF, firm or any other person, the limit of Rs10,000 will only

Firms:

- A firm is taxable at the rate of 30 percent for the assessment year 2019- Surcharge is 12 per cent of income-tax if net income exceeds Rs 1 crore. Health and Education Cess – 4% of income tax inclusive of surcharge

Income from property held for charitable or religious purposes:

- It is proposed to insert a new Explanation to the section 11 to provide that for the purposes of determining the application of income under the provisions of sub-section

(1) of the said section, the provisions of sub-clause (ia) of clause (a) of section 40, and of sub-sections (3) and (3A) of section 40A, shall, mutatis mutandis, apply as they apply in computing the income chargeable under the head “Profits and gains of business or profession

Accordingly, where a payment by an entity registered under section 11 is made in cash for more than Rs 10,000 as provided in sub-section 3 and (3A) of section 40, the cash so paid will be considered as a taxable income of such registered entity.

Likewise, where the payments made by an entity registered under section 11 requires withholding of tax and such tax is not withheld, the payment so made will not be considered as accumulation of income as per the provisions of section 40(a) /(ia) and will be chargeable to tax.

Similar, explanation is proposed to be inserted in section 10(23C) of the Act.

The above provision is proposed to be applicable from assessment year 2019-20.

Corporates:

- Corporate Tax Rate

i] Domestic Companies having total turnover or gross receipts not exceeding Rs. 250 crores in Financial year 2016-17 shall be liable to pay tax at 25% as against present ceiling of Rs. 50 crore in Financial year 2015-1

| Company | AY 2019-201 |

| Where its total turnover or gross receipt during the previous year 2016-17 does not exceed Rs. 250 crores | 25% |

| Where its total turnover or gross receipt during the previous year 2016-17 exceeds Rs. 250 crores | 30% |

| any other domestic company | 30% |

ii] No proposed change in the tax rate of foreign company (i.e. 40% plus applicable surcharge and health & education cess).

11. No change in surcharge rate

| Company | If net income does not

exceed Rs.1 Crore |

If net income is in the range of Rs.1 Crore – Rs

10 crore |

If net income exceeds Rs.10 Crore |

| Domestic Company | – | 7% | 12% |

| Foreign Company | – | 2% | 5% |

In other cases (including sections 115-O (dividend distributed), 115QA (buy-back of shares), 115R (distributed income to unit holders), 115TA (distributed income to investors) or 115TD (tax on accreted income of trusts and institutions)), the surcharge shall be levied at the rate of twelve per cent.

12. Deemed dividend

- Currently, deemed dividend under section 2(22)(e ) of the Act, is taxable in the hands of shareholders as per the applicable marginal rate. It is proposed to tax the deemed dividend in the hands of the company as part of divided distributed under section 115-O of the Act and is proposed to be taxed @ 30%. The proposed rate of 30% shall be the final rate and will not be further grossed up as is done in case of other dividend covered under the provisions of section 115-O of the

The above provisions are proposed to be applicable on transactions undertaken on or after 1 April 2018.

- A new Explanation 2A proposed to be inserted under section 2(22) (e ) of the Act, to include the accumulated profit of the amalgamating company as on date of amalgamation as well to compute the total accumulated profit for taxing deemed dividend.

13. Business Connection

a) Section 9 of the Act provides the instances where income is deemed to accrue or arise in India. It includes the income which accrues or arise in India through a business connection in India. Explanation 2 to sub-section 1 of section 9 provides the inclusive definition of business connection. Clause (c ) of the explanation provides that any business activity carried out through a person who, acting on behalf of non-resident habitually exercises in India, an authority to conclude contracts on behalf of non-resident will be treated as a business connection in India. Accordingly, the income so derived from such business connection is taxable in

It is proposed to amend provide that “business connection” shall also include any business activities carried through a person who, acting on behalf of the non- resident, habitually concludes contracts or habitually plays the principal role leading to conclusion of contracts by the non-resident. However, the such contracts will be taxable in India only if the contracts should be-

i) in the name of the non-resident; or

ii) for the transfer of the ownership of, or for the granting of the right to use, property owned by that non-resident or that the non-resident has the right to use; or

iii) for the provision of services by that non-resident.

The above amendment is proposed to be in line with BEPS Action Plan 7 have now been included in Article 12 of Multilateral Convention to Implement Tax Treaty Related Measures

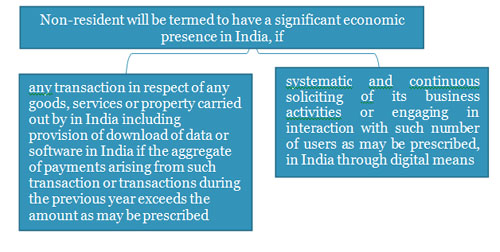

b) Currently, section 9 of the Act provides for physical presence-based2nexus rule for taxation of business income of the non-resident in India. Therefore, it is always litigated that emerging business specially in digitized businesses, which do not require physical presence of itself or any agent in India, is not covered within the scope of clause (i) of sub-section (1) of section 9 of the Act. Accordingly, there income even if generated from India, is not taxable in

To curb the above situation, it is proposed to introduce the concept of ‘significant economic presence’ in India.

The income of non-resident where the significant economic presence is established will be taxable in India only to the extent of the income attributed to such transaction (as falling in above two conditions) in India. Further, the significant economic presence will not be dependent upon the existence of residence or place of business of non-resident or the fact that no service is rendered in India.

The above amendment will not override the provisions of the Double Taxation Avoidance Agreements unless a specific amendment is made therein.

It is important to note that the government has already introduced the concept of equalization levy to withhold taxes on payment made for online advertisement, any provision for digital advertising space or any other facility or service for the purpose of online advertisement to non-residents not having any permanent establishment in India. The above step is in furtherance to it.

The above amendments are proposed to be applicable from Assessment year 2019- 20.

14. Section 10(48A) of the Act, subject to certain conditions, provides an exemption to non-resident companies where the income is accruing or arising in India on account of storage of crude oil in a facility in India and sale of crude oil in India. The exemption from tax is currently available only in completion of contract and thus in case of termination of contracts, the sale proceeds of leftover is taxable in India. The amendment is proposed to include the event of termination of contract also as eligible condition for allowing the exemption on the proceeds of leftover

15. Section 28 of the Act is proposed to be amended to include any compensation received or receivable, whether revenue or capital, in connection with the termination or the modification of the terms and conditions of any contract relating to the business of the assessee.

Accordingly, any receipt whether capital or revenue in nature arising on account of any re-negotiation, termination or modification in the terms of the business contract shall be taxable as business income.

16.It is further proposed to amend to include the fair market value of inventory on the date of conversion of such inventory into the capital asset as business income under newly proposed clause (via) to section 28 of the Act. The fair market value so considered as business income will be treated as cost of acquisition of inventory at the time of computing capital gain on sale of (converted inventory) capital asset.

Further, clause (42A) of section 2 of Act is also proposed to provide that the period of holding of such capital asset shall be reckoned from the date of conversion or treatment.

17.Section 43(5) of the Act provides the transactions from which the income is considered as speculative in nature. It also provides an exception list to consider various transactions as non-speculative nature even though the contracts are settled otherwise than by the actual delivery or transfer of the commodity or Clause (e) of section 45 of the Act provides that a transaction in respect of trading in commodity derivatives carried out in a recognized association which is chargeable to commodities transaction tax will not be considered as speculative transaction.

Currently, commodities transaction tax is payable only on non-agricultural commodity derivatives thereby leaving agricultural commodity products to be out of ambit of commodities transaction tax. Accordingly, the transactions in agricultural commodity products is treated as speculative transaction

It is proposed to include agricultural commodity products as well liable for commodities transaction tax and thus to be considered as non-speculative transaction from Assessment Year 2019-20.

18.Section 79 of the Act provides for carry forward and set off of losses in case of certain companies. It provides that carry forward and set off of losses in a closely held company shall be allowed only if there is a continuity in the beneficial owner of the shares carrying not less than 51 of the voting power, on the last day of the year or years in which the loss was incurred.

The Companies undergoing reconstruction or rehabilitation undergo change in shareholding which extends to more than 51% of the voting power. It is proposed to relax the rigors of section 79 in case of such companies, whose resolution plan has been approved under the Insolvency and Bankruptcy Code, 2016, after affording a reasonable opportunity of being heard to the jurisdictional Principal Commissioner or Commissioner. The amendment will be applicable from Assessment Year 2018-19.

19.Section 80 JJA of the Act provides additional deduction of an amount equal to 30 percent of additional employee cost incurred for three assessment Additional

employee is defined to include an employee who has been employed during the previous year and whose employment has the effect of increasing the total number of employees employed by the employer as on the last day of the preceding year.

However, the following employee are not eligible to be considered for this benefit—

- an employee whose total emoluments are more than twenty-five thousand rupees per month; or

- an employee for whom the entire contribution is paid by the Government under the Employees’ Pension Scheme notified in accordance with the provisions of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 (19 of 1952); or

- an employee employed for a period of less than 240 days during the previous year; or

- an employee who does not participate in the recognized provident fund

Further, the minimum number of employment period for apparel industry is 150 days instead of 240 days. It is proposed to reduce the minimum number of employment period for footwear and leather industry as well from 240 days to 150 days.

There were instances where the minimum employment period of 240 days is not met by the employee in the year of employment. Thus, it is also proposed to extend benefit for a new employee who is employed for less than the 240 days during the year of employment but continues to remain employed for the minimum period in subsequent year.

20.Section 80P of the Act provides 100% deduction in respect of profit of cooperative society which provide assistance to its members engaged in primary agricultural activities.

The similar benefit is proposed to be extended to Farm Producer Companies (FPC). Accordingly, a new section 80PA is proposed to be inserted to provide deduction in respect of certain income of producer companies having a total turnover up to Rs. 100 Crore, whose gross total income includes any income from-

- the marketing of agricultural produce grown by its members, or

- the purchase of agricultural implements, seeds, livestock or other articles intended for agriculture for the purpose of supplying them to its members, or

- the processing of the agricultural produce of its members

The benefit shall be available for a period of five years from the financial year 2018-19.

Presumptive Taxation

21. Special Provision for Computing profits and gains of business of plying, hiring or leasing goods carriages.

Section 44AE of the Act provides special provisions for computing profits and gain of business of plying, hiring or leasing goods carriages. Currently, the profits and gains shall be deemed to be an amount equal to seven thousand five hundred rupees per month or part of a month for each goods carriage or the amount claimed to be actually earned by the assessee, whichever is higher.

The only condition for applicability of the benefit is that the assessee should not have owned more than 10 goods carriages at any time during the previous year.

It is proposed to amend section 44AE of the Act to provide that, in the case of heavy goods vehicle (more than 12MT gross vehicle weight), the income would deemed to be 1,000 rupees per ton of gross vehicle weight or unladen weight, as the case may be, per month or part of a month for each goods vehicle or the amount claimed to be actually earned by the assessee, whichever is higher. The vehicles other than heavy goods vehicle will continue to be taxed as per the existing rates.

For other than heavy goods vehicle, the existing value of 7,500 rupees for every month or part of a month during which the goods carriage is owned by the assessee in the previous year or an amount claimed to have been actually earned from the vehicle, whichever is higher will continue.

The expressions “goods carriage”, “gross vehicle weight”, “heavy goods vehicle” and “unladen weight” are also proposed to be defined to provide clarifications. The above amendment will be applicable from assessment year 2019-20.

Alternate Taxes

22. As per section 115JB of the Act, while computing book profit, a Company is allowed to claim a deduction in respect of the amount of loss brought forward or unabsorbed depreciation, whichever is less as per books of However, in case any of the two i.e. loss brought forward or unabsorbed depreciation is Nil, the deduction is also reduced to Nil.

Post implementation of Insolvency and Bankruptcy Code, 2016 many rehabilitating companies are seeking insolvency resolution. Thus, it is proposed to allow the Companies which have filed the application for corporate insolvency resolution process under the Insolvency and Bankruptcy Code, 2016 and the application has been admitted by the Adjudicating Authority, deduction of sum total of loss brought forward and unabsorbed depreciation to the extent of book profit. The proposed amendment is applicable from assessment year 2018-19.

23.There are special provisions enacted under the Act which provide for determination of income of foreign company or non-residents on particular basis. The income derived from the source covered by the respective provision and computed in accordance with such provision shall be deemed to be the Profit and Gains of such business chargeable to tax under the head “Profit and Gain of Business or

It was always litigated that profit calculated under presumptive income provision is nevertheless income computed in accordance with the provision of this Act under the head income from Business or Profession and thus tax payable on such presumptive income together with income under other heads shall be compared with tax payable under section 115JB of the Act and then the liability shall be determined.

A retrospective clarificatory amendment (applicable from assessment year 2001-02) is proposed in section 115JB of the Act to provide that the provisions of section 115JB of the Act shall not be applicable and shall be deemed never to have been applicable to an assessee, being a foreign company, if its total income comprises solely of profits and gains from business referred to in section 44B or section 44BB or section 44BBA or section 44BBB and such income has been offered to tax at the rates specified in the said sections.

24.Alternate Minimum Tax payable by a unit located in an International Financial Service Center under section 115JC of the Act, is proposed to be reduced to 9% as against current applicable rate of 18.5%.

Penal Provisions

25.Section 276CC of the Act provides penal provisions where a person willfully fails to furnish in due time the return of fringe benefits which he is required to furnish under sub-section (1) of section 115WD or by notice given under sub-section (2) of the said section or section 115WH or the return of income which he is required to furnish under sub-section (1) of section 139 or by notice given under clause (i) of sub-section (1) of section 142 or section 148 or section 153A, he shall be punishable,

- in a case where the amount of tax, which would have been evaded if the failure had not been discovered, exceeds 25 lac rupees, with rigorous imprisonment for a term which shall not be less than 6 months, but which may extend to 7 years and with fine;

- in any other case, with imprisonment for a term which shall not be less than 3 months, but which may extend to 2 years and with

The section provides an exception that where the tax payable by person on the total income determined on regular assessment, as reduced by the advance tax, if any, paid, and any tax deducted at source, does not exceed 3,000 rupees, the penal provisions will not be attracted.

It is proposed to withdraw the exception from Companies. Thus, in the case of willful default, the Companies may be subject to the liability as well as prosecution prescribed.

26. Section 271FA of the Act provides where a person fails to furnish a statement of financial transaction or reportable account under sub-section (1) of section 285BA of the Act, penalty of 100 rupees for every day during which such failure continues is leviable.

It is proposed to increase the penalty for non-filing financial return as required under section 285BA from Rs 100 per day to Rs. 500 per day.

27. A compliance amended has been proposed to allow assessee to file appeal before the Appellate tribunal against the order of CIT(A) under section 271J of the Act where any penalty is imposed for furnishing of inaccurate information in any report or certificate by an accountant, merchant banker or a registered

Benefit for Start-ups

28. Special Provision in respect of specified business

Finance Act 2016 inserted Section 80-IAC which provides that deduction under this section shall be available to an eligible start-up for three consecutive assessment years out of seven years at the option of the assessee, if-

- it is incorporated on or after the 1st day of April 2016 but before the 1st day of April 2019;

- the total turnover of its business does not exceed twenty-five crore rupees in any of the previous years beginning on or after the 1st day of April 2016 and ending on the 31st day of March 2021; and

- it is engaged in the eligible business which involves innovation, development, deployment or commercialization of new products, processes or services driven by technology or intellectual

It is proposed to extend the benefit to the to start ups incorporated on or after the 1st day of April 2019 but before the 1st day of April 2021. Further, the requirement of the turnover not exceeding Rs 25 Crore would apply to seven previous years commencing from the date of incorporation.

Currently, the term eligible business which can claim the benefit of section 80-IAC of the includes, business which involves innovation, development, deployment or commercialization of new products, processes or services driven by technology or intellectual property. It is proposed to extend the benefit and include the business engaged in innovation, development or improvement of products or processes or services, or a scalable business model with a high potential of employment generation or wealth creation as well.

The above amendment is proposed to be applicable from Assessment Year 2018-19.

Capital Gain

29. Introduction of new section 112A to tax long term capital gain arising on sale of equity-oriented fund or a unit of a business trust

- Section 10(38) of the Act provides exemption on long term capital gain arising on sale of equity shares. It is proposed to withdraw exemption under section 10(38) in respect of transfer listed Securities Transaction Tax (“STT”) paid equity shares or a unit of an equity-oriented fund or a unit of a business trust transferred on or after 1 April 201

- A new section 112A is proposed to be introduced to tax long term capital gains arising from transfer of long term asset e. equity share in a company or a unit of an equity-oriented fund or a unit of a business trust.

- The gain under section 112A shall be taxed at 10 per However, the tax will be computed on the capital gain exceeding one lakh rupees.

- The concessional rate of 10 per cent will be available without providing the benefit of

- Further, the equity shares sold or acquired shall be those on which the STT is already paid. Thus, the tax under section 112A shall be over and above STT paid/deducted.

- The cost of acquisitions in respect of the long-term capital asset acquired by the assessee before the 1st day of February 2018 shall be deemed to be the higher of –

- the actual cost of acquisition of such asset; and

- the lower of –

- the fair market value of such asset3; and

- the full value of consideration received or accruing as a result of the transfer of the capital

3 (a) in a case where the capital asset is listed on any recognized stock exchange, the highest price of the capital asset quoted on such exchange on the 31st day of January 2018. However, where there is no trading in such asset on such exchange on the 31st day of January 2018, the highest price of such asset on such exchange on a date immediately preceding the 31st day of January 2018 when such asset was traded on such exchange shall be the fair market value; and

b) in a case where the capital asset is a unit and is not listed on recognized stock exchange, the net asset value of such asset as on the 31st day of January 2018.

30.STT at the time of transfer of long term capital asset, being a unit of equity -oriented fund or a unit of business trust, shall not apply if the transfer is undertaken on recognized stock exchange located in any International Financial Services Centre (IFSC) and the consideration of such transfer is received or receivable in foreign currency.

31.It can be understood through an example:

| Particulars | Amount in INR | |

| Shares sold on or before 31 March 2018 | Nil | Nil |

| Shares purchased before 31 January 2018 but sold after 31 March 2018 | ||

| Purchase Price where share purchased before 31 January 2018 | 100 | 100 |

| Highest price as on 31 January 2018 | 130 | 110 |

| Sale Price as on 1 April 2018 | 110 | 130 |

| Total LTCG as on 1 April 2018 | 20 | 20 |

| Exempt LTCG | 20 | 10 |

| Taxable LTCG | Nil | 10 (tax @ 10%) |

32.Tax on STT paid long term capital Gain will be 10% under Section 112 Further, where the total income comprises of long term capital gain taxable under section 112A and income under the other heads, the deduction under Chapter VIA4 will be restricted to the income under the other heads. Similarly, no rebate under section 87A of the Act will be available on such long-term capital gain income.

33.As per section 115R of the Act, income distributed by the specified company or a Mutual Fund to its unit holders of equity-oriented funds, is not chargeable to It is proposed that where dividend is distributed by a Mutual Fund being, an equity-oriented fund, the mutual fund shall be liable to pay additional income tax at the rate of ten per cent on income so distributed. The amendment is to bring all equity-oriented funds in line with the provisions of proposed section 112A of the Act.

34.Similarly, post introduction of section 112A, long term capital gain earned by FIIs on equity-oriented funds under currently exempt under section 115AD, will also be chargeable to tax at 10 per cent only in respect of amount of such gains exceeding one lakh rupees.

4 Section 80C, 80CCD, 80D, 80EE etc

35. It is proposed to amend section 47 of the Act to include the following transactions not to be considered as transfer by a non-resident for computing capital gain. However, the transaction shall be undertaken on a recognized stock exchange located in any International Financial Services Centre:

- bond or Global Depository Receipt, as referred to in sub-section (1) of section 115AC; or

- rupee denominated bond of an Indian company; or

- derivative

Further, the consideration for the transfer shall be paid or payable in foreign currency.

36.Section 50C of the Act provides that where the consideration received or accruing as a result of the transfer by an assessee of a capital asset, being land or building or both, is less than the value adopted or assessed or assessable by any authority of a State Government (hereafter in this section referred to as the “stamp valuation authority”) for the purpose of payment of stamp duty in respect of such transfer, the value so adopted or assessed or assessable shall, for the purposes of computing capital gain, be deemed to be the full value of the consideration received or accruing as a result of such transfer.

Provision of Section 50C is also proposed to be amended to allow a variation up to 5% of sale consideration in comparison to stamp duty value.

However, where the variation between sale consideration and stamp duty value is more than 5% of the sale consideration, the taxability of differential sum will continue both in the hands of seller as well as buyer.

| Particulars | Pre Amendment | Post Amendment |

| Sale Price | 86,00,000 | 86,00,000 |

| Stamp Duty Value | 90,00,000 | 90,00,000 |

| Fair Market Value as per valuer | 75,00,000 | 75,00,000 |

| Difference in Stamp Duty value and sale price | 400,000 | 400,000 |

| Variation % on sale price | 4.65% | 4.65% |

| Capital Gain as on 1 April 2018 | 400,000 | Nil (variation being less than 5% of sale

price) |

37.Section 54EC of the Act provides benefit of capital gain exemption if investment in specified Bonds is made. It is proposed to restrict the exemption only if Capital gain is arising from sale of land and building only. Further period of holding being increased from 3 years to 5 years. By means of this amendment it has been proposed is to withdraw exemption hitherto available in respect of all other capital assets such as shares, jewellery etc.

Method of Accounting 5

38.Section 145 of the Act empowers the Central government to notify Income Computation and Disclosure Standards (“ICDS”). In pursuance the central government has notified ten such standards effective from 1st April 2017 relating to Assessment year 2017-1These are applicable to all assesses (other than an individual or a Hindu undivided family who are not subject to tax audit under section 44AB of the said Act) for the purposes of computation of income chargeable to income-tax under the head “Profits and gains of business or profession” or “Income from other sources”.

In order to bring certainty in the wake of recent judicial pronouncements on the issue of applicability of ICDS, it is proposed to —

5 Taken as-it-is from Memorandum of Finance Act 2018.

- amend section 36 of the Act to provide that marked to market loss or other expected loss as computed in the manner provided in income computation and disclosure standards notified under sub-section (2) of section 145, shall be allowed

- amend 40A of the Act to provide that no deduction or allowance in respect of marked to market loss or other expected loss shall be allowed except as allowable under newly inserted clause (xviii) of sub-section(1) of section

- insert a new section 43AA in the Act to provide that, subject to the provisions of section 43A, any gain or loss arising on account of effects of changes in foreign exchange rates in respect of specified foreign currency transactions shall be treated as income or loss, which shall be computed in the manner provided in ICDS as notified under sub-section (2) of section 1

- insert a new section 43CB in the Act to provide that profits arising from a construction contract or a contract for providing services shall be determined on the basis of percentage of completion method except for certain service contracts, and that the contract revenue shall include retention money, and contract cost shall not be reduced by incidental interest, dividend and capital gains.

- amend section 145A of the Act to provide that, for the purpose of determining the income chargeable under the head “Profits and gains of business or profession, —

- the valuation of inventory shall be made at lower of actual cost or net realizable value computed in the manner provided in income computation and disclosure standards notified under (2) of section 1

- the valuation of purchase and sale of goods or services and of inventory shall be adjusted to include the amount of any tax, duty, cess or fee actually paid or incurred by the assessee to bring the goods or services to the place of its location and condition as on the date of

- inventory being securities not listed, or listed but not quoted, on a recognised stock exchange, shall be valued at actual cost initially recognised in the manner provided in income computation and disclosure standards notified under (2) of section 14

- inventory being listed securities, shall be valued at lower of actual cost or net realizable value in the manner provided in income computation and disclosure standards notified under (2) of section 145 and for this purpose the comparison of actual cost and net realizable value shall be done category-wise.

- insert a new section 145B in the Act to provide that

- interest received by an assessee on compensation or on enhanced compensation, shall be deemed to be the income of the year in which it is received.

- the claim for escalation of price in a contract or export incentives shall be deemed to be the income of the previous year in which reasonable certainty of its realisation is

- income referred to in sub-clause (xviii) of clause (24) of section 2 shall be deemed to be the income of the previous year in which it is received, if not charged to income tax for any earlier previous

Country-by-Country Reporting

39. Section 286 of the Act contains provisions relating to specific reporting regime in the form of Country-by-Country Report (CbCR) in respect of an international group. 31 March 2018 will be the due date for filing of first CbCR for financial year 2016-1 Following clarificatory amendments to be in line with Rules already prescribed are proposed to be made so as to improve the effectiveness and reduce the compliance burden of such reporting

- the time allowed for furnishing the Country-by-Country Report (CbCR), in the case of parent entity or Alternative Reporting Entity (ARE), resident in India, is proposed to be extended to twelve months from the end of reporting accounting year. Currently, the time prescribed is on or before due date of filing of

- constituent entity resident in India, having a non-resident parent, shall also furnish CbCR in case its parent entity outside India has no obligation to file the report of the nature referred to in sub-section (2) in the latter’s country or territory;

- the time allowed for furnishing the CbCR, in the case of constituent entity resident in India, having a non-resident parent, shall be twelve months from the end of reporting accounting year;

- the due date for furnishing of CbCR by the ARE of an international group, the parent entity of which is outside India, with the tax authority of the country or territory of which it is resident, will be the due date specified by that country or territory;

- Agreement would mean an agreement referred to in sub-section (1) of section 90 or sub-section (1) of section 90A, and also an agreement for exchange of the report referred to in sub-section (2) and sub-section (4) as may be notified by the Central Government;

- “reporting accounting year” has been defined to mean the accounting year in respect of which the financial and operational results are required to be reflected in the report referred to in sub-section (2) and sub-section (4).

Assessment

40. Finance Act 2018 proposes a new procedure for scrutiny assessment under section 143(3) of the Act. It is also proposed to insert two new provisions under sub-section (3A) and (3B) of section 143 for enabling the government to prescribe the new scheme for scrutiny assessments or any modification therein, by way of notification in the Official

However, such modifications/directions shall be issued up to 31 March 2020.

41. Sub-clause (vi) of Sub-section (1) of section 143(1) provides for adjustment in respect of addition of income appearing in Form 26AS or Form 16A or Form 16 which has not been included in computing the total income in the

It is proposed to insert a new proviso to the said clause to provide that no adjustment under sub-clause (vi) of the said clause shall be made in respect of any return furnished on or after the assessment year commencing on the first day of April 2018. The amendment will be applicable for Assessment Year 2018-19.

Others

42.PAN as (Unique Entity Number) to be obtained by all entities including HUF other than individuals in case aggregate of financial transaction in a year is Rs 2,50,000 or more. All directors, partners, members of such entities also to obtain

43. For AY 2019-20 – Education cess (2%) and Secondary Education cess (1%) discontinued. However, a new cess by the name of Health and Education cess levied @ 4% levied on tax inclusive of

44.Deductions in respect of certain incomes provided under Chapter VIA – Part C of the Act shall not be allowed unless the return of income is filed by the due Deduction under Chapter VIA includes specific deductions provided under section 80IA, 80IB, 80 IAC, 80JJA containing special benefits provided. The proposed amendment will be effective from assessment year 2018-19.

45.Under the existing provisions of the clause (12A) of section 10 of the Act, an employee contributing to the NPS is allowed an exemption in respect of 40% of the total amount payable to him on closure of his account or on his opting out. This exemption is not available to non-employee In order to provide a level playing field, it is proposed to amend clause (12A) of section 10 of the Act to extend the said benefit to all subscribers.

46.At present, similar to the provisions of section 50C of the Act, while taxing income from business profits (section 43CA) and other sources (section 56) arising out of transactions in immovable property, the sale consideration or stamp duty value, whichever is higher is adopted. The difference is taxed as income both in the hands of the purchaser and the seller. Provision of Section 43CA and 56(2)(x) is also proposed to be amended to allow a variation up to 5% of sale consideration in comparison to stamp duty

However, where the variation between sale consideration and stamp duty value is more than 5% of the sale consideration, the taxability of differential sum will continue both in the hands of seller as well as buyer.

47.Interest on compensation, enhanced compensation. Claim or enhancement claim and subsidy, incentives to be taxed in the year of receipt only as per new Section 14

48.National Technical Research Organization (“NTRO”) is proposed to be exempted from withholding on the payments in the nature of Royalty or fees for technical services covered under section 195. Accordingly, a new clause 6D is proposed to be inserted under section 10 of the Act exempting NTRO from withholding any tax.

49. Section 140 of the Act is proposed to be amended to provide that during the resolution process under the Insolvency and Bankruptcy Code, 2016, the return shall be verified by an insolvency professional appointed by the Adjudicating Authority under the Insolvency and Bankruptcy Code, 201

50. New Rules – Rule 1 to Rule 11 for computing agricultural income referred in sub-clause

-

- of Clause (1A) of Section 2 of the Act proposed. In consonance with the rules proposed, agricultural income proposed to be computed considering it as income chargeable to income-tax under the Act under the head “income from other sources” and deductions provided under section 57 to 59 shall

1 plus applicable surcharge and health & education cess

2 Either in the form of business connection, permanent establishment or place of effective management